Exploring the Rise of NFT Liquidity

May 16th, 2022

Disclaimer: FLYING FALCON HAS INVESTED IN DIGITAL LAND AND NFTS. THIS STATEMENT IS INTENDED TO DISCLOSE ANY CONFLICT OF INTEREST AND SHOULD NOT BE MISCONSTRUED AS A RECOMMENDATION TO PURCHASE DIGITAL LAND, NFTS OR ANY TOKEN. THIS CONTENT IS FOR INFORMATIONAL PURPOSES ONLY AND YOU SHOULD NOT MAKE DECISIONS BASED SOLELY ON IT. INVESTING IN ANY CRYPTO ASSET IS A MAJOR RISK. THIS IS NOT INVESTMENT OR FINANCIAL ADVICE.

INTRODUCTION:

NFTs had a breakout year and led the crypto asset class adoption during 2021 by nearly any measure.

- $17.6 billion traded in total (21,350% growth year-over-year)

- $27.4 million in total sales (1,836% growth year-over-year)

- 2.57 million total active wallets (1,822% growth year-over-year)

- $16.9 billion total market capitalization (4,440% growth year-over-year)

Source: NonFungible.com Yearly NFT Market Report 2021

While growth has been remarkable, there remain critical pieces of infrastructure that must be built to help push the NFT asset class forward. One which seems most obvious, and one we have been monitoring closely, is efficient borrowing and lending markets around NFTs. Product market fit has been demonstrated for fungible tokens through lending protocols like Aave and Compound. Additionally, non-fungible assets IRL, such as real estate, art and collectibles, have extensive debt markets. It would make sense that NFTs would follow.

We are keeping a close eye on the growth of NFT debt markets. It’s important to us, as owners of 13 genesis land plots in Axie Infinity we eye a future where we can borrow against our cash-flow generating land, unlocking more capital for the open metaverse more broadly. More generally, for digital nations to emerge to their full potential, we must create methodologies for the owners of assets to unlock liquidity without requiring the full disposal of the underlying NFT. This additional capital extracted from the underlying NFTs can then be funneled back into the ecosystem, accelerating the growth and production of these digital nations.

What follows in this paper is a deep dive on NFTfi, which, in our view, is leading the pack in the emerging NFT lending market space.

What is NFTfi?

NFTfi, founded by Stephen Young in 2019, is a peer-to-peer NFT lending platform built on Ethereum. The platform connects owners of NFTs seeking to borrow against their assets with lenders of liquidity seeking yield opportunities.

“Our main focus is that we want to do for NFTs what DeFi did for cryptocurrencies. As soon as you brought DeFi into cryptocurrencies, you also had this explosion of activity and liquidity in the market. And really, we want to act as that catalyst for the NFT market, unlocking some of the value in these NFT’s so they can then be ploughed back into the NFT community and market to help develop the space further.” – Stephen Young (Source)

Borrowers are generally individuals that seek capital to cover short-term capital expenditures or aim to perform a trading strategy that, in their view, can outperform their cost of capital on the loan. In both scenarios, borrowers are able to unlock liquidity without selling their sentimentally valued NFT. We believe that with growth and adoption, we will see a scenario where borrowers are representatives of NFT native DAOs such as Flamingo and Pleasr who have treasuries composed of NFTs. An adoption such as this would drastically increase the NFT collections on such lending and borrowing protocols. This will offer more assets for lenders to lend against along with a plethora of liquidity for DAOs that have been classified as illiquid based on their treasury holdings.

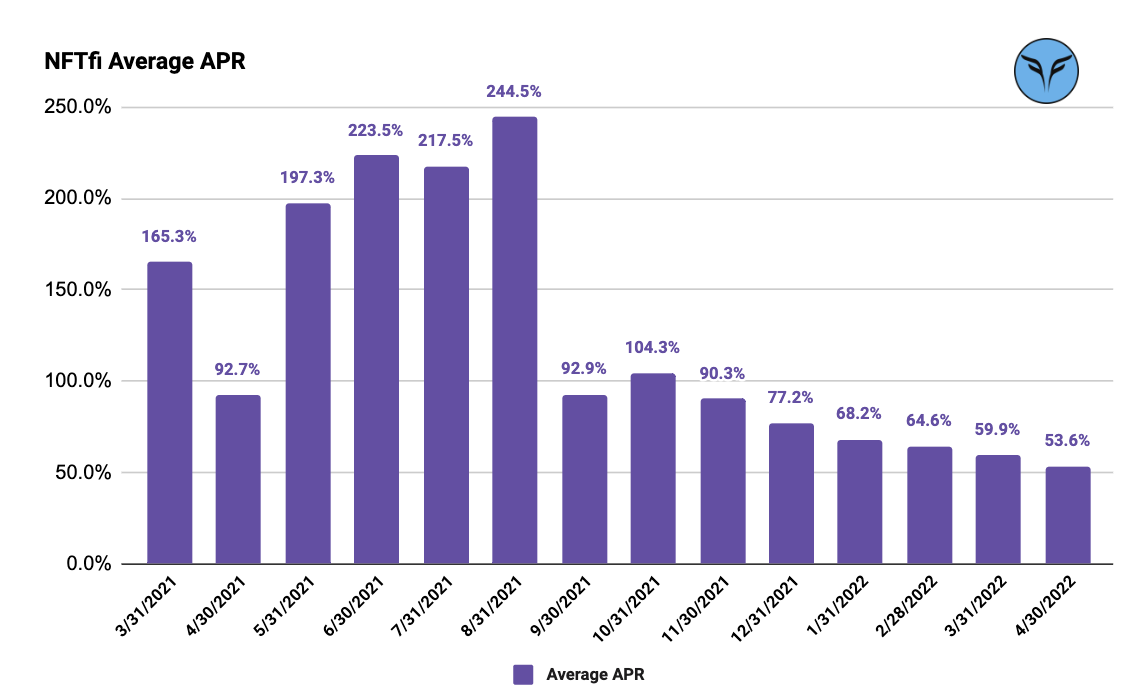

On the lending side of the equation, lenders are typically individuals comfortable lending against an NFT as collateral along with DAOs that are underwriting loans and providing the necessary liquidity to earn a yield. Over the course of NFTfi’s lifetime, the APR has averaged 375%,100%, 65% and 37% across 7 day, 14 day, 30 day and 90 day periods. We have already seen the APR average trend down and we expect that with even greater adoption and natural competition, APRs will continue to decrease and find a relative equilibrium for each loan duration.

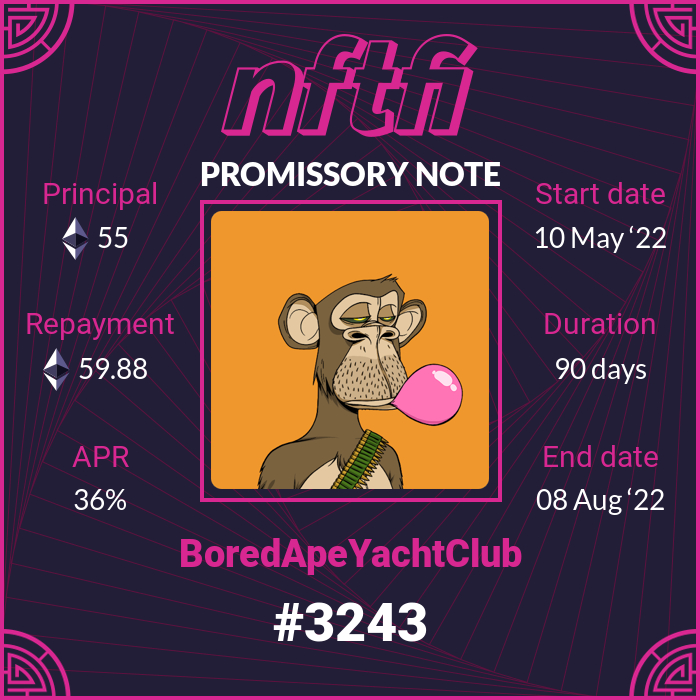

The platform ultimately connects unacquainted individuals (peer to peer) and generates loan agreements without the typical intermediaries. Once a loan is agreed upon by the two parties, the borrower deposits their NFT as collateral in an escrow account and receives the respective loan. Simultaneously, the lender mints a NFT which NFTfi refers to as their promissory note, or a tangible representation of the loan terms. The loan terms such as the principal, repayment, APR, start date, duration and end date are all clearly identified on the NFT promissory note. If the loan were to expire prior to the borrower depositing the repayment amount, the lender would have the right to redeem the promissory note and receive the NFT from escrow.

It is important to highlight that NFTfi functions as peer to peer rather than peer to pool. In the fungible DeFi space, peer to pool has led the market in growth with the likes of Aave and Compound. There are various reasons to believe why a peer to peer protocol is the optimal model over a peer to pool platform for most NFTs. First, peer to pool requires a reliable oracle which is difficult for non-fungible tokens, and even with the development of a secure NFT oracle, it would likely be limited to floor NFTs and would treat each NFT in a collection pari-passu. This would severely limit the growth for the rarer NFTs within a collection. Additionally, many market participants have an emotional connection to their NFT, especially for pfps and rare collectibles. Some participants would continue to pay their loan even if their NFT collateral fell below the loan amount. Lenders may also be willing to negotiate with the borrower and extend the duration or payment terms to avoid liquidation. As such, defaults should only happen when the borrower misses a payment, which bodes better for peer to peer markets.

Growth and the Market Opportunity

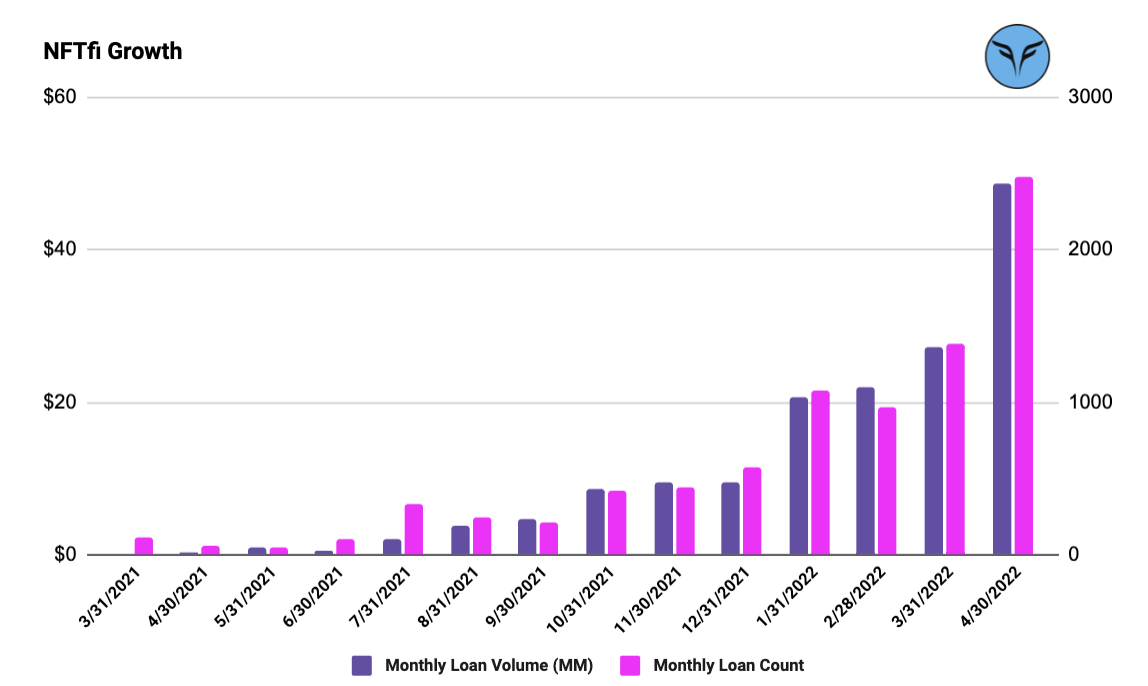

Over the prior 12 months, NFTfi’s monthly loan volume increased from less than $1 million to over $47 million and monthly loan count increased from less than 100 to over 2,400 unique loans. Important to note that this growth happened without direct token incentives, though perhaps some volume is being inflated by market participants’ hope of a retroactive airdrop. We believe the major catalyst for this rise was the general wider acceptance and growth of NFT valuations. Over the coming months, better educational materials for borrowers and more sophisticated lenders will be critical for sustained growth.

We expect to see attractive protocol revenue dynamics as volumes rise, especially when benchmarked against the fungible DeFi lending space. This is largely due to the higher interest rates commonly associated with less liquid assets that require a level of sophistication. In April 2022, the average APR was 54%, which compares to 3.4% for the Aave protocol. We expect the 54% to continue to come down materially as markets become more efficient, though the term length loans and illiquidity of the underlying asset will likely always command a relatively high interest rate.

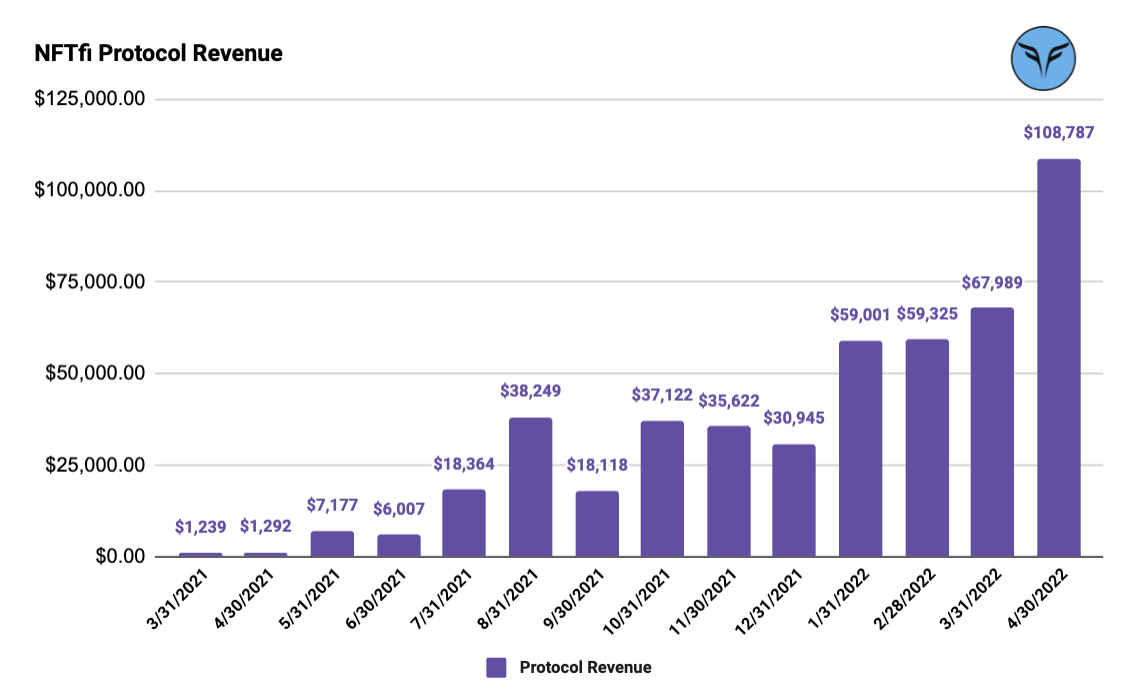

In April 2022, the 54% APR on $47M of loan volume resulted in approximately $2.1M of total interest paid on the platform. Important to note, NFTfi receives a 5% take rate on this total interest, which in the case of April 2022 resulted in ~$109,000 of protocol revenue ($1.3M annualized). For comparison purposes, Aave receives approximately ~10% on average as its take rate which suggests that the 5% take rate for NFTfi may be reasonable longer term and perhaps can even increase. Additionally, NFT marketplaces such as OpenSea tend to be around 5% which again suggests 5% is a market competitive take rate.

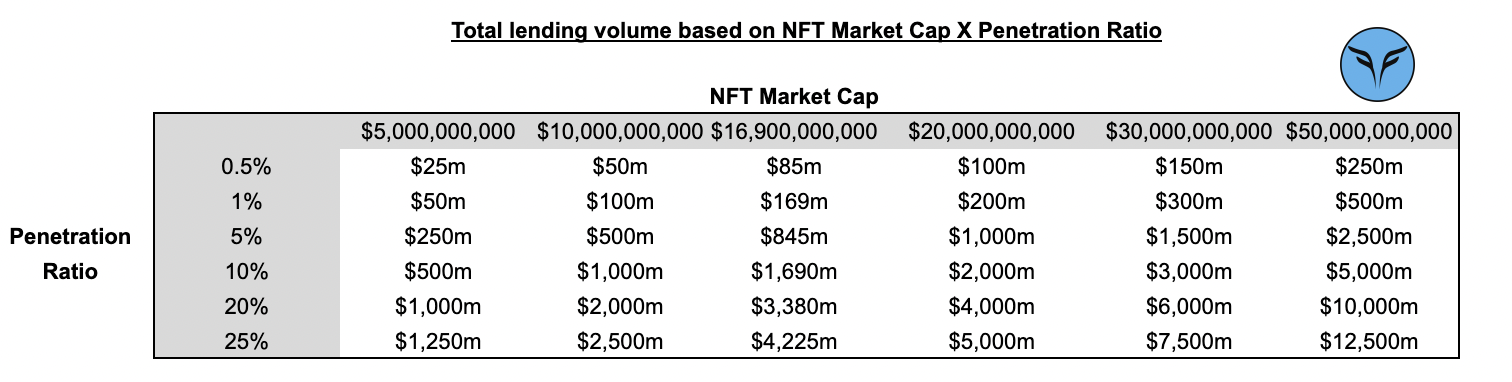

A critical component to NFTfi’s future revenue growth is underlying loan volume growth, which we believe has room to grow substantially. NFTfi’s lending volume annualized (based on Q1 2022) represents approximately 1.5% of the total NFT market cap (as of 2021). This penetration rate is extremely low when benchmarked across traditional art and mortgage markets (Source). At the current NFT market cap, should penetration rates reach 10%, this would result in $1.7B of annualized lending volume. If the NFT market cap reached $30B at this same 10% penetration rate, this would result in $3B of annualized lending volume. The potential market here seems massive. See sensitivity table below.

We believe the largest future potential for NFTfi lending volume is the proliferation of productive gaming and land assets. One current dilemma, at present, is the owner of game assets do not have the ability to borrow against their asset on NFTfi and utilize their asset in-game simultaneously. This effectively means all assets within NFTfi forfeit their ability to be cash flow productive. This would be as if a property owner couldn’t both take out a mortgage and rent out their property, for example.

When this is inevitably solved and as blockchain games and virtual worlds mature further, we believe these productive game assets and land become the most common form of collateral as the underlying cash flow mitigates the risk for the lender and provides more familiar valuation techniques. For example, as we discussed in our piece on digital land, we believe land as a gaming asset can generate substantial cash-flow in the form of in-game resources, game tokens, and governance tokens, along with SDK monetization and advertisements. In theory, collateralizing an asset like this should provide the lender with a greater margin of safety given the projected cash-flows and longer term can be valued in traditional ways such as a discounted cash flow model. For large owners of these game assets, such as guilds and gaming organizations, borrowing against these assets can increase capital efficiency and accelerate growth.

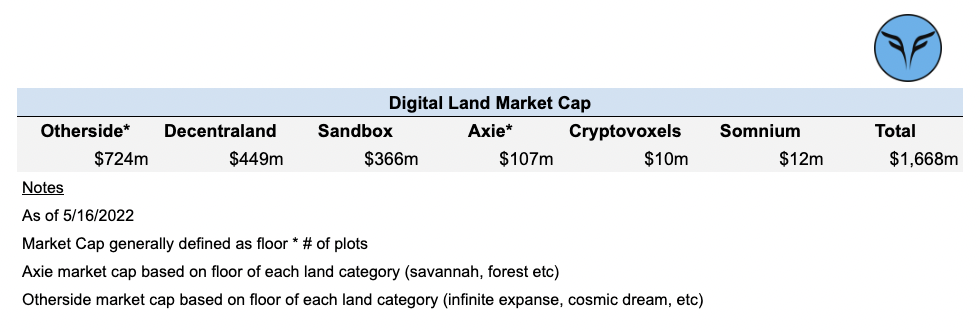

At present, there is approximately $1.67 billion worth of digital land across the prominent metaverses. As these become more established with cash-flows beginning to generate, this is significant potential loan volume for lenders. At a potential LTV of 40%, this would result in $668M of loans at current valuations and unlock significant capital to be invested back into the respective nations.

Conclusion

The NFT lending and borrowing ecosystem is one we are closely monitoring and participating in. Most importantly, we believe the NFT lending space has the potential to accelerate the growth of digital nations as liquidity can be unlocked from the underlying assets and invested back into the respective economy. We want to see this future unfold and we are here to help.

We view NFTfi as the leader in the space while simultaneously keeping an eye on potential competitors as the industry continues to evolve. The industry is extremely nascent and niche, though we believe a combination of NFT market growth, enhanced UX, better education, the rise of gaming assets, and more sophisticated lenders will push volume higher. Lastly, and a topic we have saved for a future paper, we believe the formation of liquidity provider DAOs that make lending as easy as depositing a stable coin in a Yearn Finance vault will be a critical step to unlocking the full potential of NFTfi.

As always, please reach out to us if you want to discuss ideas presented here further.

Additional Resources:

Jason Choi Podcast: Source

Zima Red Podcast: Source

Delphi Digital Podcast: Source

NFTfi Website: Source

NFTfi Twitter: Source

NFTfi Loan Bot: Source